Discover how these three countries are overcoming challenges and fostering economic growth against all odds. A compelling read awaits you!

Table of Contents

Developing countries like Kenya, Bangladesh, and Srilanka face a myriad of economic challenges as they strive for sustainable growth and development. Despite obstacles such as poverty, political instability, and infrastructure deficits, these nations are making significant strides towards building resilient economies. Let’s explore the innovative solutions and ambitious initiatives that are propelling Kenya, Bangladesh, and Srilanka towards a brighter economic future.

Kenya: A Beacon of Hope

Kenya’s economy has been on a steady growth trajectory in recent years, driven by a diverse range of sectors including agriculture, tourism, and technology. However, the country still grapples with high levels of poverty and unemployment, as well as occasional bouts of political instability. Despite these challenges, the Kenyan government has been proactive in implementing bold reforms aimed at addressing income inequality and improving infrastructure.

One of the key strategies employed by Kenya is the promotion of entrepreneurship and innovation. The government has created a supportive ecosystem for startups and small businesses, providing access to funding, mentorship, and networking opportunities. Initiatives like the Huduma Centers, which offer a one-stop shop for government services, have streamlined bureaucratic processes and enhanced efficiency.

Bangladesh: Rising from the Ashes

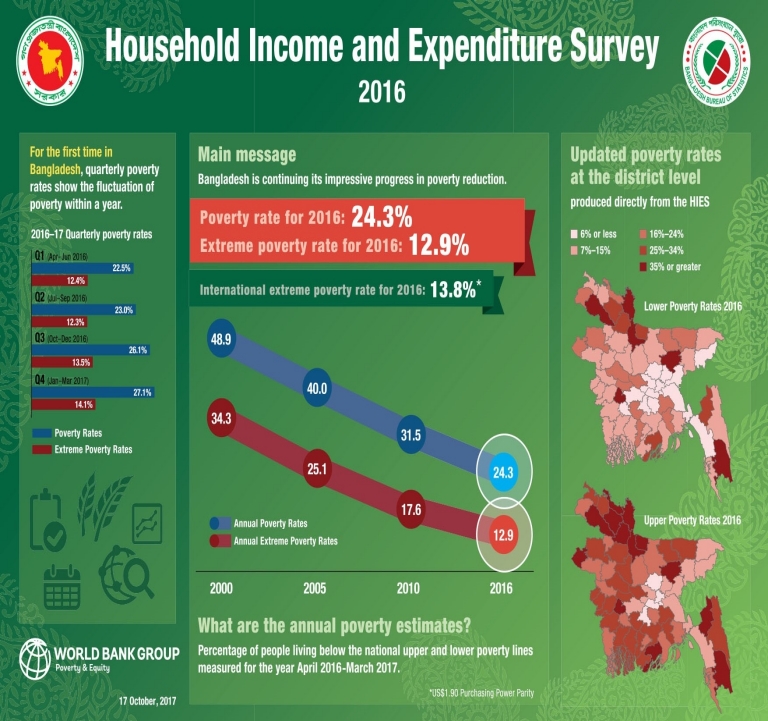

Bangladesh has emerged as a success story in economic development, with sustained growth in key sectors such as textiles, agriculture, and information technology. Despite facing challenges such as low wages and political instability, the country has implemented innovative solutions to drive economic progress and improve the quality of life for its citizens.

One of the standout initiatives in Bangladesh is the microfinance sector, which has significantly empowered women and marginalized communities by providing access to credit and financial services. Organizations like Grameen Bank have pioneered the concept of microcredit, enabling individuals to start their own businesses and lift themselves out of poverty.

Srilanka: Charting a New Course

Srilanka has undergone a period of economic transformation, with reforms aimed at attracting foreign investment, reducing debt levels, and promoting sustainable development. Despite challenges such as ethnic conflicts and environmental degradation, the country is making strides towards building a more inclusive and resilient economy.

Image courtesy of www.worldbank.org via Google Images

One of the key strategies in Srilanka’s economic revitalization is the focus on infrastructure development, particularly in the areas of transportation and energy. Projects like the Colombo Port City and the Megapolis Plan are transforming the urban landscape and creating new opportunities for growth and investment.

Final Thoughts

As we reflect on the economic challenges faced by developing countries like Kenya, Bangladesh, and Srilanka, it becomes clear that resilience, innovation, and strategic planning are crucial for sustained growth and prosperity. By implementing bold reforms, investing in human capital, and fostering a culture of entrepreneurship, these nations are paving the way towards a brighter future for their citizens and contributing to global economic development. Let us continue to support and celebrate the progress of these countries as they navigate the obstacles on the path to economic success.

Generated by Texta.ai Blog Automation